A Deep Dive into District-Level Banking in India

Analyzing Branch Size and Account Values from Hyper-Dense Metropolitan Hubs to Rural Frontiers

ANALYTICS

5/19/20264 min read

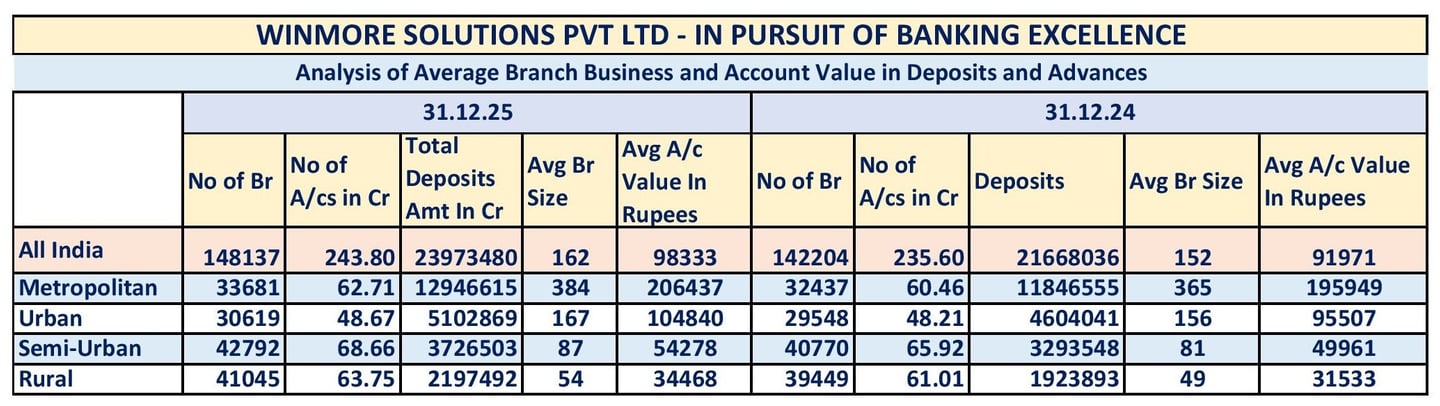

The Reserve Bank of India (RBI) classifies bank branches and centers into four population groups; metro, urban, semi-urban, rural. This categorization helps RBI to regulate banking infrastructure and ensure financial inclusion. The data presented above is the analysis of the average branch business and average account value in deposits and advances at a population level - This reveals a significant disparity between all the categories.

Metropolitan districts account for 23% of total bank branches and these centers hold a branch size (Total deposits divided by No. of branches) of 384 crores which is 2.4 times the national average.

Rural districts despite accounting for 28% of the total bank branches holds a branch size of 54 crores while the national average 162 crores. The account values also exhibits a similar pattern where the metropolitan districts command an account value which is 2.1 times higher than the national average of 98 lakhs, while rural districts barely hold 35% of the national average.

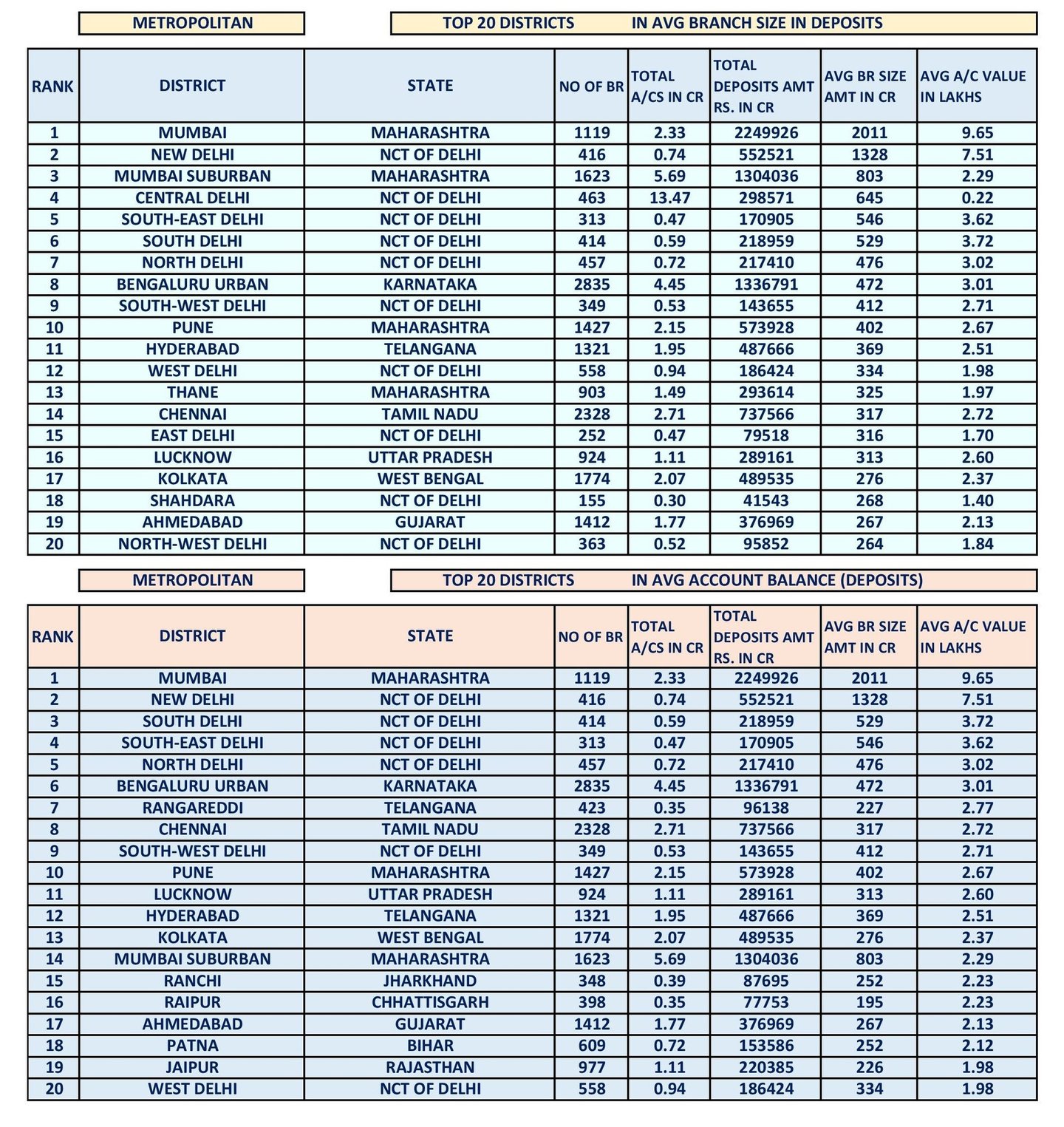

1. Metropolitan Tier : Capital Concentration

Mumbai and New Delhi, the top two metropolitan centers to report the highest average branch size and account value. Outperforming other centers by a significant margin, these center's metrics are 8 to 12 times higher than that of the national average. As the country's the financial and national capitals, they house a significant volume of high net-worth demographics this trend can be seen in the breakdown of the top metropolitan districts below.

Central Delhi has the highest concentration of accounts, which dilutes the average account value, indicating these accounts are mostly saving or low-value accounts. While Bengaluru urban and Chennai hold the highest number of branches and total accounts, they still rank within the top ten for average account value. This metropolitan data offers a clear insight into how branch concentration can influence both the branch size and account value. Meanwhile the consumer hubs like Bengaluru, Mumbai and Chennai continue to expand, driven by the growing economic activity.

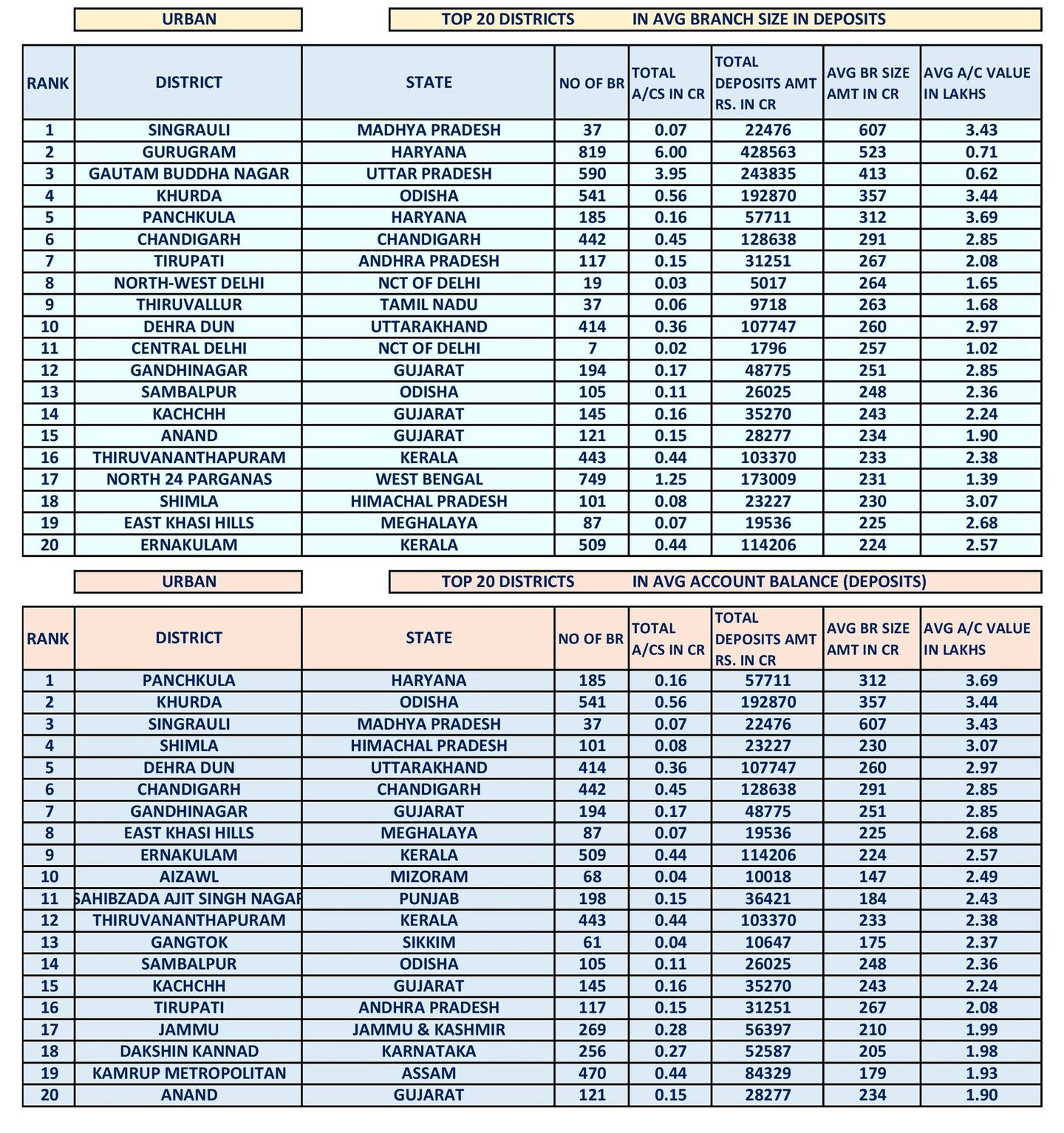

2. Urban Tier: Industrial Wealth vs. Corporate Hubs

The Urban districts dataset is reveals a completely different trend from the metropolitan dataset. Unlike the metropolitan districts, the dataset shows specific financial pockets due to industrial wealth or high income groups.

Singrauli, the 'Energy capital of India' stands as a glaring outlier. With only 37 branches, it tops the average branch size in the urban districts by a good margin and also ranks 3rd in the average account value. While the lower concentration of branches raises the average branch size, the high account value paints a picture of the highly affluent local workforce and business ecosystem. In contrast Gurugram and Gautam Buddha Nagar hold a high concentration of branches, total accounts and total deposits. Although the overall branch size remains high, the density of the branches in these districts is diluting the average account value. On the other hand, Panchkula and Khurda holds concentrated wealth centers, due to which the average account values and also branch sizes are higher for a low concentration of branches.

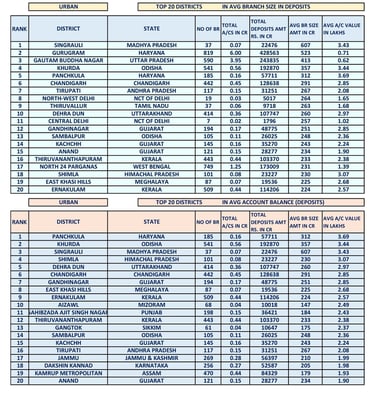

3. Semi-Urban Tier: The Reality of Fragmented Wealth

The Semi-Urban dataset reflects the brutal reality of fragmented wealth distribution across India. While these districts hold 29% of all the Bank branches in India, they only represent 14% to 16% of the population. Rather than a unified growth, dataset exposes the highly dispersed population with wealthy micro-pocket, tourism hubs and strategic locations. This demographic dispersion creates a pattern of small number of branches serving a low-density but highly affluent population, which naturally drives up both average branch size and account value.

South-West Delhi and East Delhi districts though classified as semi-urban these districts house a highly affluent diaspora dwelling in private enclaves. Their close proximity to the Indira Gandhi International (IGI) Airport reduces the branch concentration while leveraging branch size and account value. Tourism pockets like North and South Goa also exhibit an identical pattern. A rapidly growing hospitality and tourism economy contributes to the branch size. Paschimi Singhbhum district ranks 2nd in branch size shows mining activity and private enterprise growth. Tawang has only 6 branches in total yet it ranks 3rd nationally in both branch size and account value due to the geographic barriers the few branches monopolize on the local wealth.

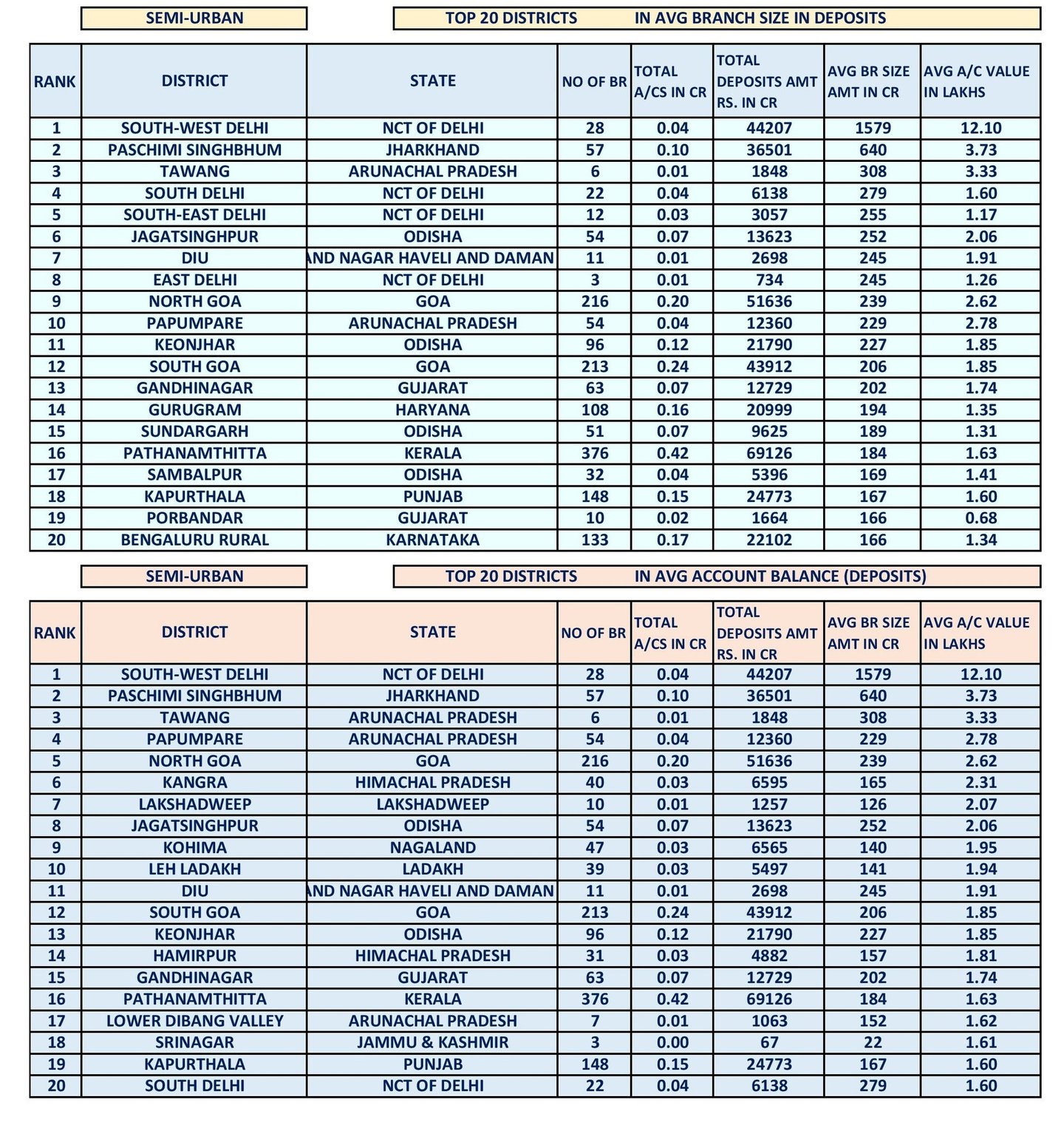

4. Rural Tier: Edge Metros

This Rural district dataset exposes remote geographical locations with sparse banking infrastructure but abundant wealth pooling. Smaller concentration of branches serving low density population, Bengaluru rural is the leader ranking number 1 in both average branch size and account value by a massive margin. Though classified as rural the geographical location makes it a lucrative business corridor and suburban townships outside Bengaluru. Tawang and Leparada due to the geographic barriers the few branches monopolize on the local wealth. North-East Delhi, West Delhi, South Delhi these branches rank high in average branch size simply because they are sitting on the urban-rural edge of the nation's capital.

Every district tells a unique story, and your growth strategy should be just as specialized. At WINMORE SOLUTIONS, we provide the strategic tools to turn these complex competitive trends into a clear, high-performance roadmap for your Banking institution.

If you are ready to stop reacting to market pressures and start leading, let’s collaborate. Contact us for a tailored, deep-dive analysis of your specific target geographies, and let us guide your bank on its next step in pursuit of banking excellence.

Get in touch

Optimizer@winmoresol.com

© 2026 by Winmore Solutions Pvt Ltd